2023 CURRENT EU

Looking at the global sector since the 2023 Almanya Intersolar Fair;

By mid-2023, there was nearly 40 GW of panel stock waiting in warehouses in the Netherlands due to unchecked material supply in response to the 2022 demand. Many Chinese companies were caught with stocks because demand was less than the related unchecked supply. According to an October 2023 article in PV Magazine,

Nearly 100 GW of unsold perc modules are waiting in European warehouses. Since the panels in stock are priced at $0.23 per watt and the current spot price has dropped to $0.15 per watt, it is uncertain what will happen to the stock panels.

On the other hand, there has been a dramatic drop in cell prices. Although there are no projects that will make a huge impact, projects in the range of 700 Kwp-1MW are progressing as multiples, and additional incentives are being provided for residential solar projects.

Looking at all of Europe;

End of 2022 Installed capacity: 208.9 GW

41.4 GW commissioned by the end of 2022

It is expected to exceed 50 GW by the end of 2023. (LOW SCENARIO: 42 GW)

Expected total installed capacity by the end of 2023 is 262 GW

The main goal is to make solar energy one of Europe's primary energy systems.

Key topics for 2030: Energy storage

In December 2022, the European Solar Industry Association was established to support local production and supply materials from Europe.

Ref: Solar Power Europe Market Outlook 22-26

GLOBAL 2022-2023

Looking at the overall global market;

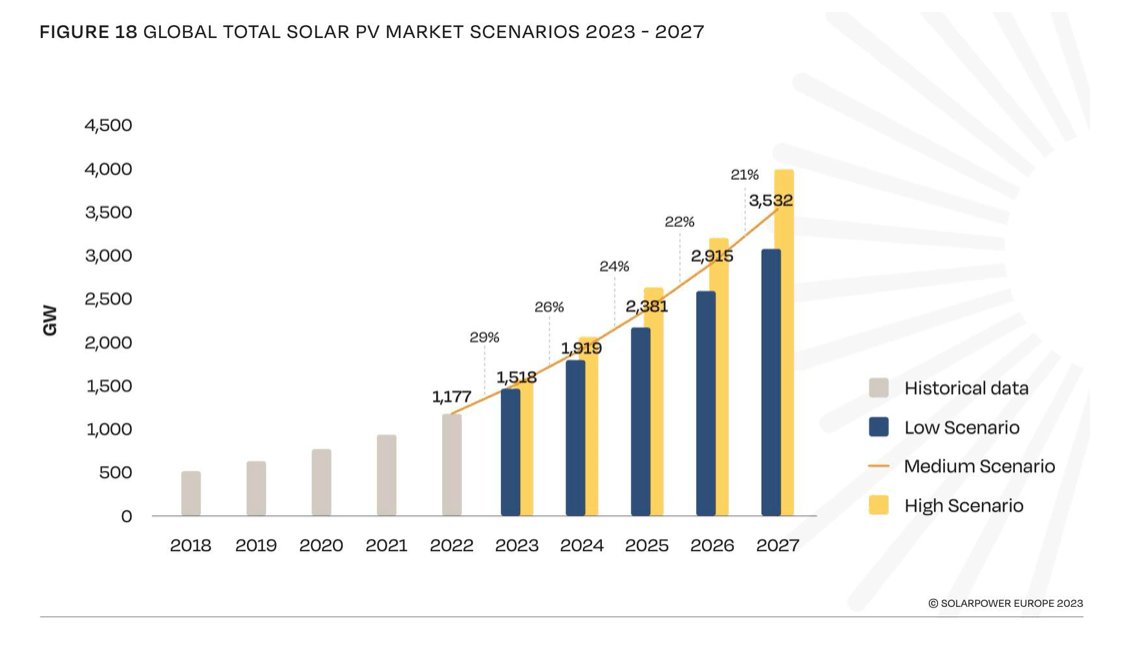

By the end of 2023, it is expected that 341 GW of capacity will be connected to the grid in the global solar market. This represents a 43% growth compared to the previous year. The high forecast for 2023 is at the level of 402 GW. At the end of 2022, global installed capacity exceeded 1 TW.

Solar energy meets about 4.5% of global energy demand. 70% of it is met by non-renewable energies.

The cost of electricity generated from solar energy, one of the cheapest sources of electricity in the world, is in the range of 50-60 USD per Mwh (1000 Kwh). Ref: Lazard April 2023

https://www.lazard.com/research-insights/2023-levelized-cost-of-energyplus/

In the global developments between 2000-2022;

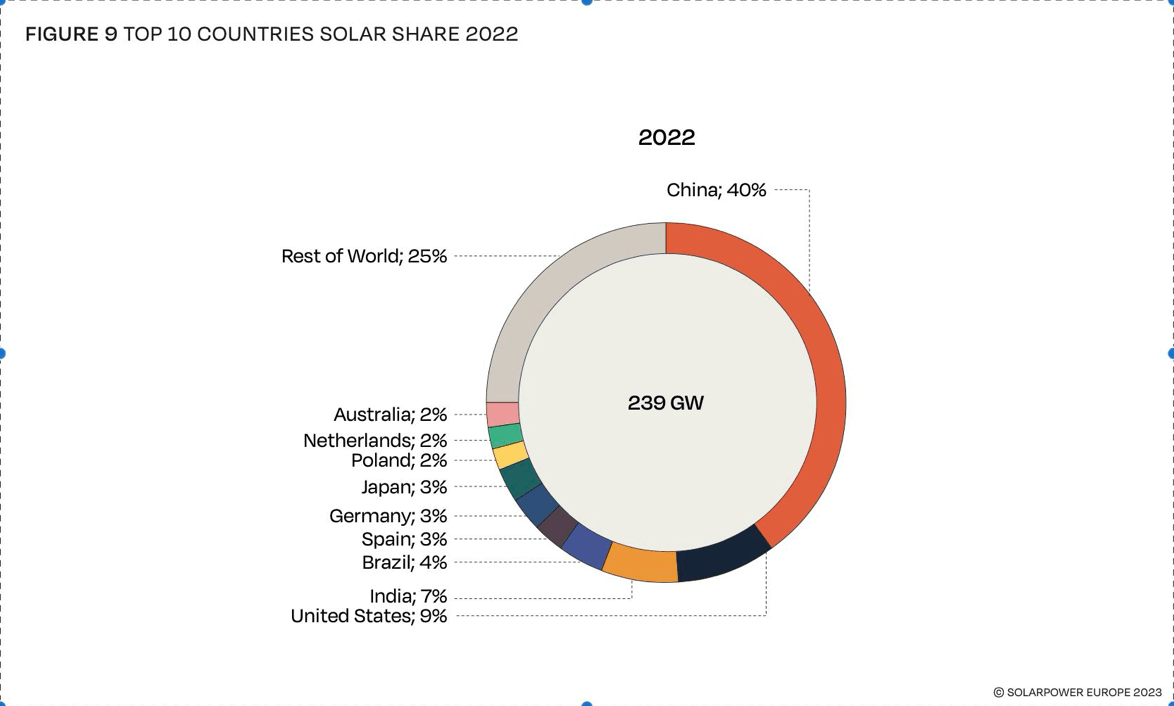

Spain, with its investments, took the third place in the Top 5 solar markets in 2022 by installing 8.4 GW. The main installations consisted mostly of PPA (bilateral agreements) and grid-scale installations. This trend is expected to continue for markets with installations of 25 GW and above in 2023, with a trend towards environmental regulations.

Germany maintained its 6th place. 7.4 GW was installed in 2022. Most of the installations were in the rooftop segment. The power of tenders with large-scale installations was increased from 750 Kw to 1 Mw. On the other hand, additional incentives were provided for homeowners to install charging and storage systems for electric vehicles.

Poland ranked 8th with 4.5 GW installed in 2022. 78% consisted of rooftop installations.

Netherlands ranked 9th with 4.1 GW installed in 2022.

China, ranked first, is expected to have an installed capacity of 95 GW to 120 GW by the end of 2023.

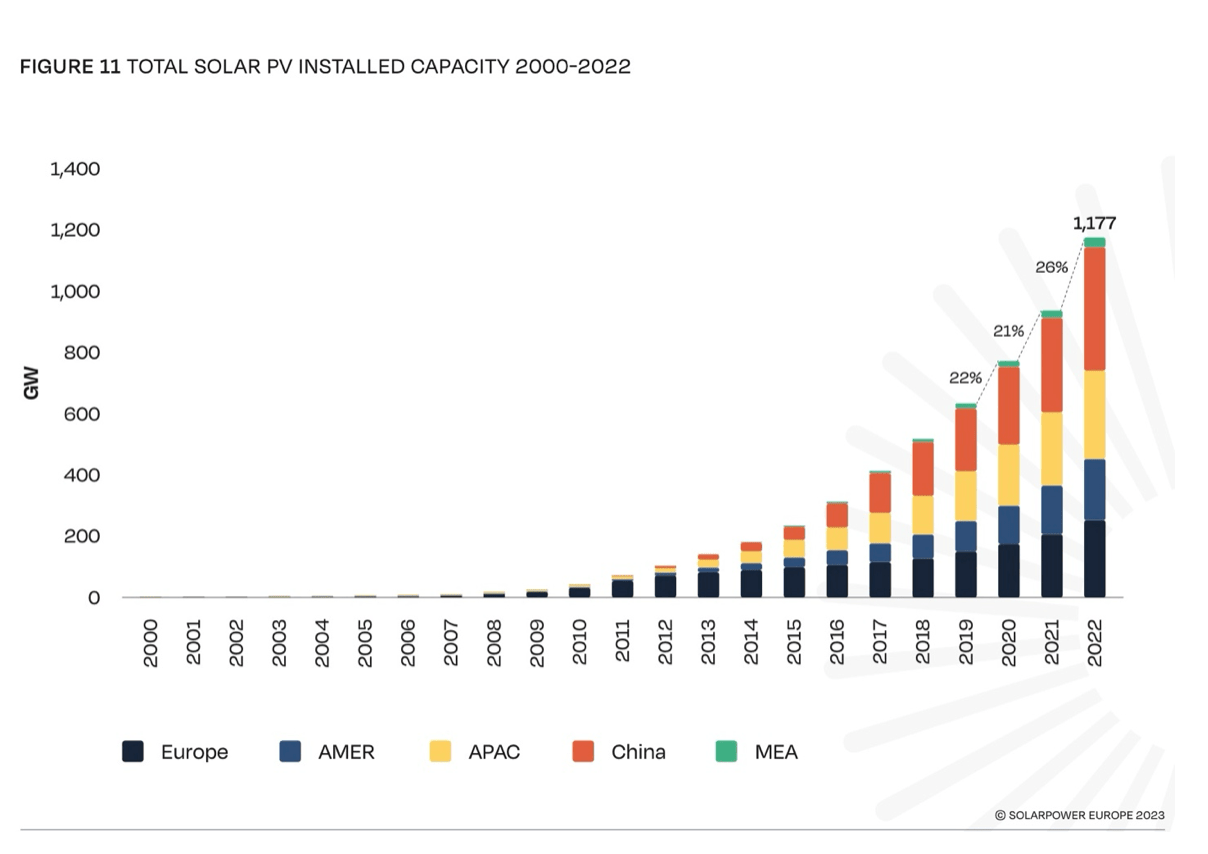

A total of 1.177 GW of installations took place worldwide. Compared to 938 GW in 2021, there was a 25% initial growth.

GLOBAL MARKET FORECAST 2023-2027

As mentioned above, it is expected that 341 GW of installations will take place worldwide by the end of 2023. The growth rate compared to 2022 will be at the level of 43%. When asked to industry experts, this figure will reach 400 GW.

Growth rates for 2024 and beyond are around 17-15%.

Europe will continue to be an important player in the solar market in 2023 and beyond.

Looking at the American market, due to the Inflation Reduction Actions (IRA) in August 2022 and the policies to become a Global Clean Energy Power, it has become a very attractive market. There have been successive announcements by large-scale producers to invest in the American market. Also, in September 2023, many manufacturers from Turkey participated by opening stands at the RE+ fair. On the other hand, it is expected that tariff exemptions for pv modules produced in Cambodia, Malaysia, Thailand, and Vietnam will be lifted in June 2024. There are around 3 panel manufacturers from Turkey that have invested or are continuing investment efforts in the American market. It is expected that the number of these manufacturers will increase every day.

You can reach the current and prospective panel manufacturers in the USA market from the relevant link.

https://www.solarpowerworldonline.com/u-s-solar-panel-manufacturers/

IRA is a historic legislation that supports both the upper and lower solar energy sectors, including the system sub-component manufacturers, in the country's clean energy policy.

Looking at the Global Economic slowdown, the world's growth rate has decreased from 2.7% to 1% and below. The IMF and World Bank Meeting in Marrakech on October 9-15, 2023, will provide a better understanding of the world's economy and growth in the last quarter.

The IMF's general prediction is that the core inflation target will be reached before 2025.

Investments that will slow down will accelerate again.

Looking at the Global Pv Market scenario;

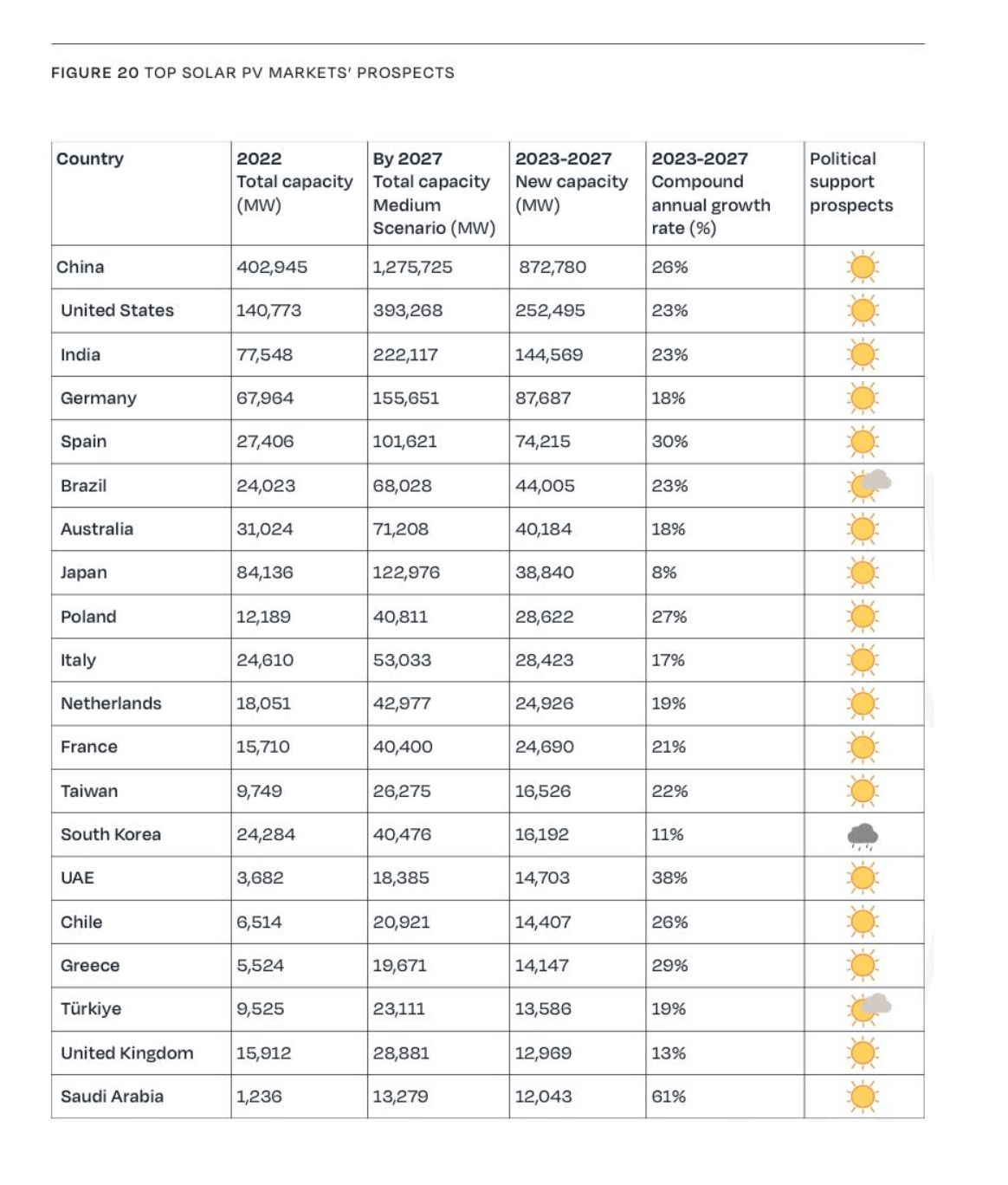

The top 4 countries in this market will be China, America, India, and Germany, respectively.

SUMMARY

Although the period between 2023 and mid-2024 is economically challenging, solar energy investments and initiatives are reaching higher levels every day in Turkey, especially. Storage GES and distributed energy will be one of the most important and cost-effective energy sources in the world. In this respect, global growth will continue at levels of 17-19%. For the next 6-7 years, solar energy and technologies will be our main agenda due to climate change and electrification transition. On the other hand, there is still no established regulation on the recycling of panels in countries or developing countries. This issue will become important in 5 years.

We hope that all conditions in the world (regulations, economy, production) will be constructive for Solar. The rest will come naturally.

Let's say the sun shines and finds its way.

Stay sunny and healthy.

Alican EKİN

Ekinler Group (Partner)

Ekinler Industries Inc.

General Manager

{kind=link}